The financial landscape of India is undergoing a massive shift this month. With the Union Budget 2026 discussions in full swing and the Income Tax Act, 2025 set to replace the decades-old Income Tax Act of 1961, taxpayers are looking at a completely new set of rules starting April 1, 2026.

For businesses, professionals, and salaried employees, the biggest changes revolve around Tax Deducted at Source (TDS). The government has finally moved to lower TDS rates for several common payments, reducing the cash-crunch faced by small businesses. At the same time, new sections like 194T have been introduced to widen the tax net.

Here is a complete, simple breakdown of the TDS updates you need to know for the financial year ending 2026 and the upcoming fiscal year.

1. The “2% TDS Club”: Big Relief for Agents and Professionals

One of the most welcome updates is the rationalization of TDS rates. To improve cash flow for service providers, the government has slashed the TDS rate from 5% to 2% on several key sections.

If you deal with commissions, brokerage, or rental payments, this is huge news. It means less tax is held back, leaving more money in your bank account during the year.

- Section 194H (Commission & Brokerage): Reduced to 2% (Earlier 5%).

- Section 194-IB (Rent by Individuals/HUF): Reduced to 2% (Earlier 5%). Note: This applies if you pay rent over ₹50,000/month and are not liable for tax audit.

- Section 194M (Contractors/Professionals): Reduced to 2% (Earlier 5%). Applies to payments by individuals for personal purposes.

- Section 194DA (Life Insurance Policies): Reduced to 2% (Earlier 5%) on the income portion of the payout.

Why this matters: Earlier, agents and small professionals often had to wait for months to claim refunds because their actual tax liability was much lower than the 5% deducted. The new 2% rate fixes this imbalance.

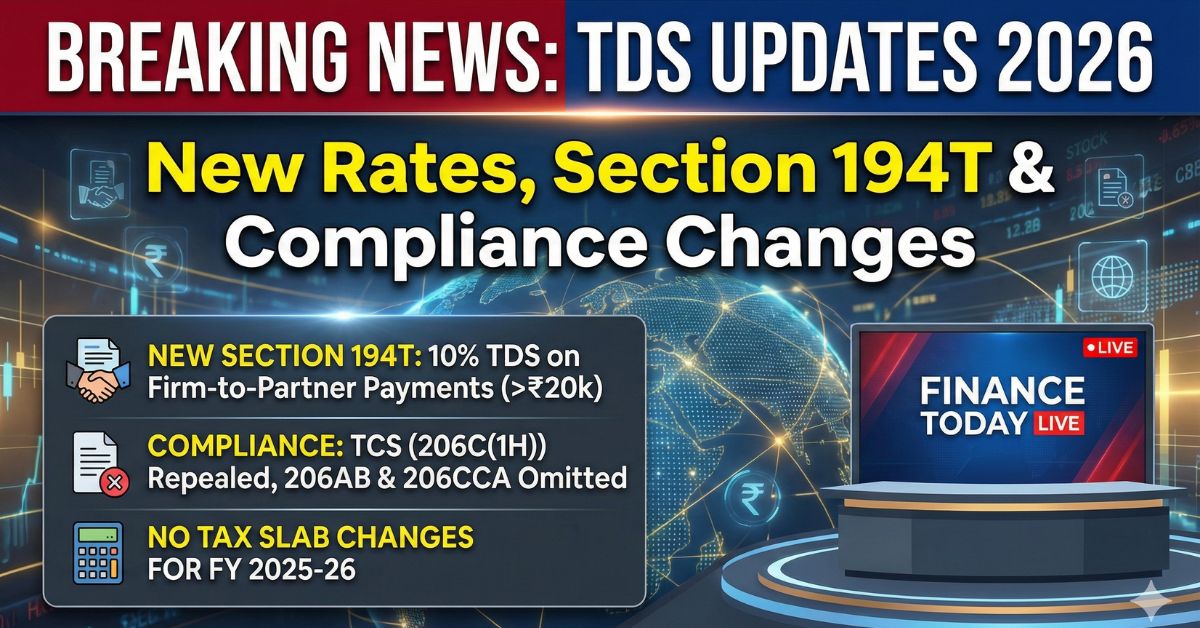

2. Section 194T: New TDS on Partners’ Income

Starting from this fiscal cycle, Partnership Firms (including LLPs) face a new compliance requirement. The government has introduced Section 194T.

- What is it? A mandatory 10% TDS on payments made by a firm to its partners.

- What payments are covered? Salary, remuneration, commission, bonus, and interest.

- Threshold Limit: TDS applies if the total payment to a partner exceeds ₹20,000 in a financial year.

This is a major change. Previously, firms simply paid partners without deducting tax. Now, they must deduct 10% and issue a TDS certificate (Form 16A), treating partners somewhat like employees for tax compliance purposes.

3. End of the “Non-Filer” Compliance Nightmare (Section 206AB)

For the last few years, businesses struggled with Section 206AB. This rule forced them to deduct double TDS if the vendor had not filed their Income Tax Returns (ITR) for previous years. It required checking the status of every vendor on the tax portal, which was a heavy compliance burden.

The recent updates propose to omit/remove Section 206AB and 206CCA.

- The Good News: You no longer need to verify if your supplier filed their ITR.

- The Impact: You can deduct TDS at normal rates (e.g., 2% or 10%) without worrying about penal rates. This significantly simplifies the accounts payable process for businesses in 2026.

4. TCS on Goods Withdrawn (Section 206C-1H)

In a move to declutter the tax system, the Tax Collected at Source (TCS) on sale of goods (Section 206C-1H) has been effectively withdrawn/merged.

Previously, there was confusion between TDS on purchase of goods (194Q) and TCS on sale of goods (206C-1H). The updates clarify that Section 194Q prevails.

- Rule: If a buyer’s turnover is over ₹10 Crore and they buy goods worth over ₹50 Lakh, they must deduct 0.1% TDS.

- Change: Sellers are largely relieved from the burden of collecting TCS on these transactions, reducing the “double compliance” confusion.

5. Updates for Salaried Employees (FY 2025-26)

For the current assessment year, TDS on salary (Section 192) is calculated based on the Revised New Tax Regime, which is now the default.

- Tax-Free Limit: Income up to ₹3 Lakh is exempt from tax.

- Rebate (Section 87A): Individuals earning up to ₹7 Lakh pay zero tax.

- Standard Deduction: Increased to ₹75,000 (up from ₹50,000).

- Family Pension Deduction: Raised to ₹25,000 (up from ₹15,000).

Employers will deduct tax based on these new slab rates unless the employee explicitly opts for the Old Tax Regime.

6. TDS on Property and E-commerce

- Property Sale (Section 194-IA): If you buy a property valued over ₹50 Lakh, you must deduct 1% TDS. Correction: If there are multiple buyers or sellers, the limit applies to the total value of the property, not individual shares.

- E-commerce (Section 194-O): The TDS rate for e-commerce operators remains at the reduced rate of 0.1% (lowered from 1% previously) to support the digital economy.

What Should You Do Next?

If you are running a business, update your accounting software immediately. Ensure your system is set to deduct 2% for brokerage/rent instead of 5%, and start tracking payments to partners for Section 194T. For salaried individuals, check your payslips to ensure the Standard Deduction of ₹75,000 has been factored into your TDS calculations.

Read More : AI Daily Assistants in 2026

Frequently Asked Questions (FAQs)

Q1: When do the new reduced TDS rates (2%) apply?

The reduced rates for commission (194H), rent (194-IB), and professionals (194M) are effective from the start of the financial year mentioned in the Finance Act (typically April 1).

Q2: Is TDS applicable on partner’s salary in a partnership firm?

Yes. Under the new Section 194T, firms must deduct 10% TDS if the payment (salary, interest, bonus) to a partner exceeds ₹20,000 in a year.

Q3: Do I still need to check if my vendor filed their ITR for TDS?

No. The compliance burden of Section 206AB (higher TDS for non-filers) has been removed to simplify business operations. You can deduct TDS at normal rates.

Q4: What is the TDS rate for buying a house in 2026?

If the property value is above ₹50 Lakh, the buyer must deduct 1% TDS on the total sale price before paying the seller.

Q5: Has the Standard Deduction changed for salaried employees?

Yes, the Standard Deduction has been increased from ₹50,000 to ₹75,000 under the New Tax Regime, lowering your taxable salary.